For years, the global benchmark for data privacy has been the General Data Protection Regulation, often referred to as GDPR. It fundamentally changed how companies across the world think about personal data because its violations can lead to heavy fines of up to €20 million or 4% of annual global revenue. This has shifted the balance of power from organisations to individuals, making consent, transparency, and accountability non-negotiable.

India is now at a similar inflection point.

With the introduction of the Digital Personal Data Protection Act (DPDPA), 2023, along with the DPDP Rules 2025, the India data protection law is moving towards a consent-first, privacy-centric digital economy.

Among all industries, the lending ecosystem is expected to undergo one of the most significant transformations under the DPDP Act. Built on extensive use of personal and financial data, the whole cycle of lending workflows that involves customer acquisition to collections will need to be fundamentally rethought in a DPDP-powered DPD-driven world.

If you’re a business with Indian customers, or your mobile app or website is accessible to them, it’s crucial to familiarise yourself with India’s new data protection legislation. But first, let’s understand what exactly is personal data, the foundation of the DPDP Act.

What is personal data under the Indian privacy law?

The Digital Personal Data Protection Act 2023 defines personal data as:

“Any data about an individual who is identifiable by or in relation to such data.”

This definition is intentionally broad as it encompasses any information that directly or indirectly can be used to identify an individual, whether on its own or when combined with alternative data.

In the context of the financial ecosystem, almost everything qualifies as personal data:

- Lead data (phone number, name)

- KYC data (PAN, Aadhaar)

- Bank statements

- Credit bureau reports

- Collection call logs, and others

This means every stage of borrower interaction is now to be regulated.

Now that we know what personal data is, let’s get straight into what the DPDP Act is.

What is India’s Digital Personal Data Protection Act (DPDP Act)?

Consent.

Personal data must be collected only with clear, informed consent, no more ambiguous or forced checkboxes buried in terms & conditions.

India’s Digital Personal Data Protection (DPDP) Act, 2023, along with the DPDP Rules 2025, marks a fundamental shift in how organisations collect, process, and manage personal data. The law introduces strict requirements around security safeguards for entities handling personal data.

Let’s examine several key provisions that strengthen borrower data protection while restricting unchecked use of personal data:

- Focus on digital personal data: The Act applies specifically to digital personal data, including data that may be collected offline but is subsequently digitised, bringing most modern lending operations under its scope.

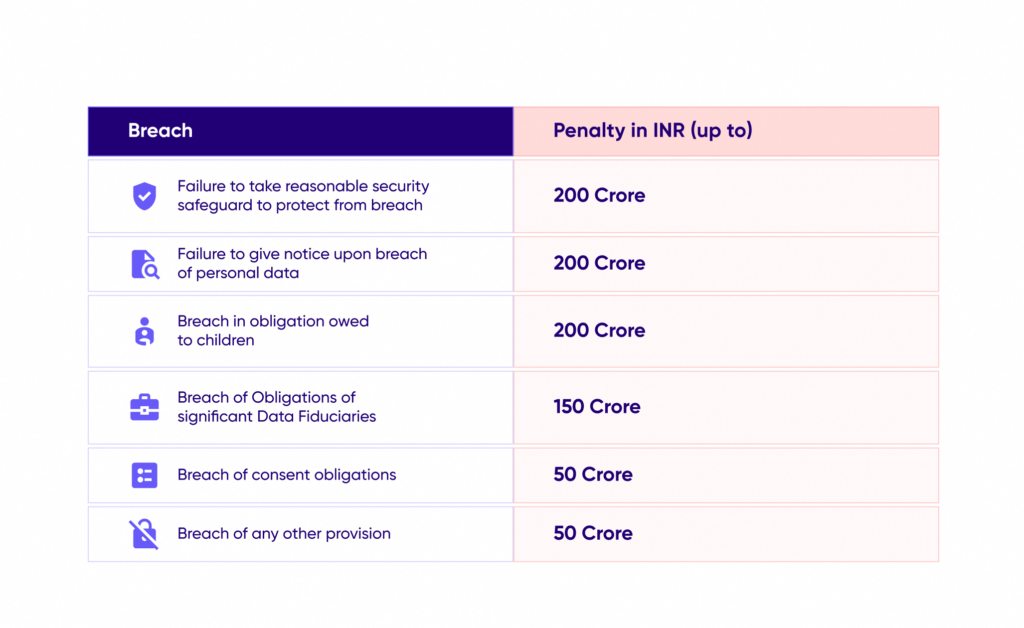

- Significantly higher penalties: Non-compliance can attract steep fines of up to ₹250 crore, making data protection a board-level priority for lenders and fintechs.

- Introduction of duties for data principals: While the Act empowers individuals, it also introduces accountability, including penalties for filing false or frivolous complaints, ensuring balanced responsibility.

- Updated framework for cross-border data transfer: The Act enables international data flows but under government-notified restrictions, requiring companies to be more cautious about where and how borrower data is stored or processed globally.

- Stronger Consent management and exemption guidelines: Consent management must now be clear, specific, and purpose-driven, with limited and well-defined exemptions, as this significantly reduces the scope for vague or blanket data usage practices.

Who are the important parties to the India DPDP Act?

At the core of the DPDP Act lies a structured framework of key participants who interact with personal data. Understanding these roles is critical, as the India data protection law assigns specific obligations and rights to each party involved in the lifecycle of data processing:

Data principal (data subject)

A Data Principal is the individual to whom the personal data belongs. In the case of minors, their parents or legal guardians act as the data principal. Similarly, for individuals with disabilities, their legally appointed guardian represents them in matters related to personal data.

Data fiduciary (data controller)

A Data Fiduciary is any entity that determines the purpose and means of processing personal data. This can include a wide range of organisations, such as startups, small businesses, financial institutions, or banks that collect and use personal data in their operations.

Data processor

A Data Processor is an entity that processes personal data on behalf of a data fiduciary. It does not decide how or why the data is used but carries out processing activities as instructed by the fiduciary.

Significant data fiduciary (SDF)

A Significant Data Fiduciary (SDF) is a data fiduciary that is specifically classified by the Central Government based on factors such as the scale and sensitivity of data processed, and potential risks to national interests or public systems like electoral democracy.

Appointing a Data Protection Officer (DPO) and a data auditor who conducts regular impact assessments and data audits, etc., is also a compulsion.

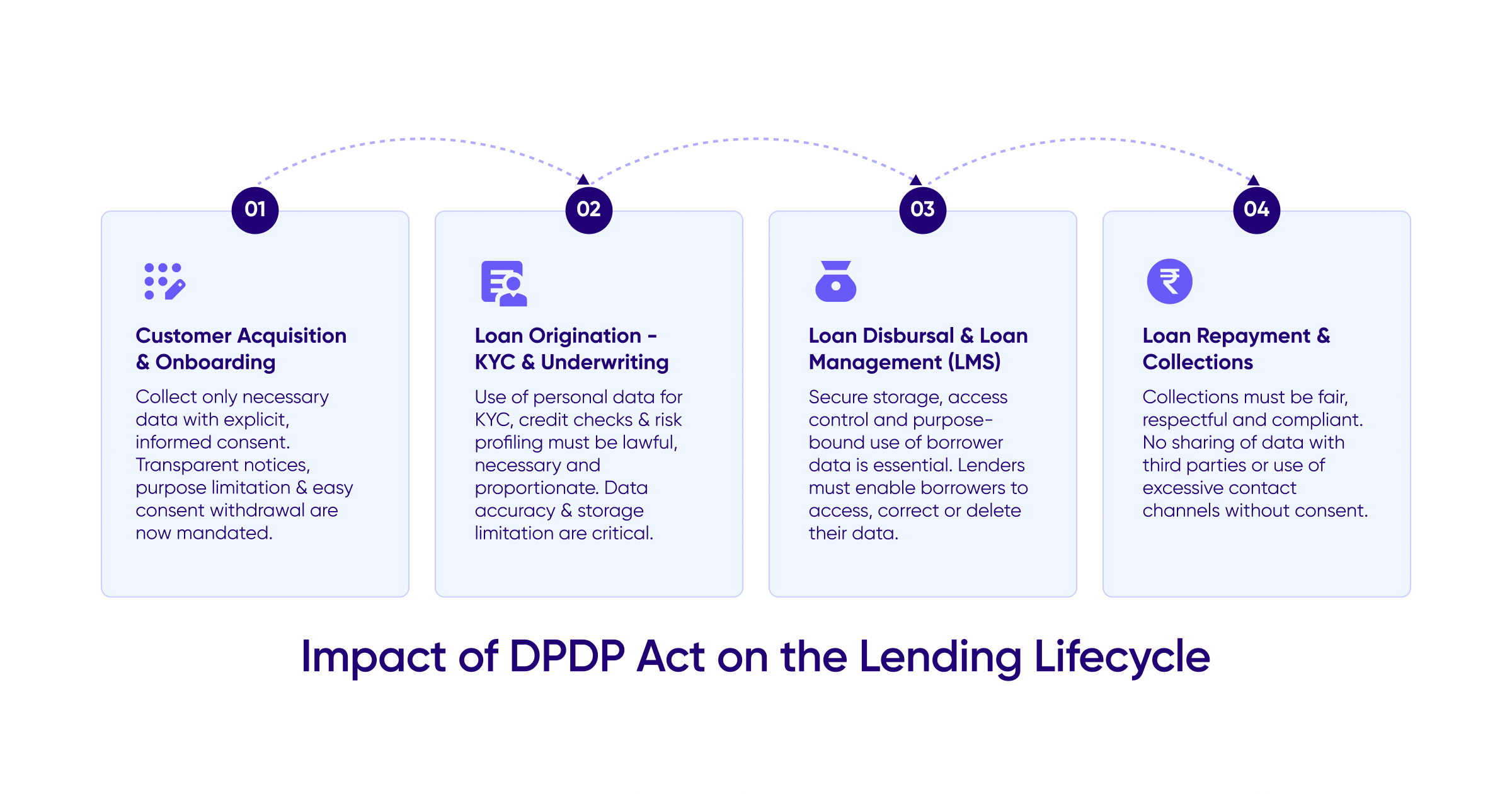

Impact of DPDP Act on the Lending Lifecycle

For the lending ecosystem, which operates almost entirely on borrower data like identity, financial behavior, credit history, and repayment patterns, this regulation will significantly reshape how digital lending operates across its lifecycle.

The lending ecosystem is divided broadly into 4 categories:

- Customer Acquisition & Onboarding

- Loan Origination – KYC and Underwriting

- Loan Disbursal & Loan Management Systems (LMS)

- Loan Repayment & Collections

Let’s understand one by one the impact on each of the above steps of the lending lifecycle.

Customer Acquisition & Onboarding

Customer acquisition is the first touchpoint in the lending ecosystem, where lenders collect lead data and initiate borrower onboarding through digital channels, DSAs, marketplaces, or fintech apps. Under the DPDP Act, lead data itself is considered personal data, and therefore cannot be collected or used without clear consent from the individual.

Key Changes:

1. Consent-first acquisition: Fintech lenders will no longer be able to rely on ambiguous or bundled consent mechanisms. Consent must be clear, purpose-specific, and revocable. This means:

- Lead marketplaces must maintain clean consent trails

- Customers must know why their data is being collected

- Consent cannot be reused across unrelated purposes

2. Restrictions on aggressive data collection: Historically, many lending apps relied on phone metadata, SMS scraping, contact list access, etc. However, the DPDP Act prohibits such intrusive practices, forcing lenders to rely on more transparent data sources.

Impact

For lenders, the customer acquisition becomes more compliant, but definitely slower, as now the marketing funnels will rely on explicit approval from the user. In the long run, this shift will reduce unauthorised data access and thereby improve borrower trust in digital lending platforms.

Loan Origination (KYC & Underwriting)

Loan origination is the stage where lenders collect financial and identity data to assess borrower risk.

This stage includes:

- KYC verification

- Credit bureau checks

- Bank statement analysis

- Income verification

- Underwriting models

Because underwriting relies heavily on sensitive personal data, the DPDP Act introduces major governance requirements.

Key Changes

1. Purpose-bound data processing: Borrower data must only be used for the specific purpose for which consent was provided. For example, KYC data cannot be reused for marketing, and underwriting data cannot be reused for cross-selling without consent

2. Data minimisation: Lenders will need to collect only the data necessary for risk assessment, forcing many fintech underwriting models to be redesigned, as currently underwriting models rely on alternative signals. But under DPDP, these data sources will need clear user consent and strong justification.

Impact

With underwriting being under strict rules, it won’t be wrong to say that the pipelines will have much cleaner data, stronger audit trails, and underwriting models wherein privacy is a built-in thing by design.

Loan Disbursal & Loan Management Systems (LMS)

Once a loan is approved, lenders use Loan Management Systems (LMS) to manage the disbursal, servicing, and monitoring of loans. These systems store highly sensitive borrower information, including repayment schedules, bank account details, contact information, communication logs, and more.

With the DPDP act focusing strongly on data storage, security, and access control, it’s important for LMS platforms to pivot in their outreach strategies.

Key Changes

1. Stronger data security requirements: Organisations must implement reasonable security safeguards that include encryption, access controls, audit logs, and breach reporting protocols.

2. Data retention limits: Borrower data cannot be retained indefinitely. Data must be deleted once the purpose is completed, or when consent is withdrawn, and can be retained only if required by other regulatory obligations.

Impact

Lenders will need to work with LMS platforms that work in compliance with the latest regulations because lenders are always under the ambit of the RBI. Right from privacy architecture to a lifecycle-based data deletion, and strict role-based access, LMS needs this type of infrastructure.

Loan Repayment & Collections

The repayment and collections stage is one of the most data-sensitive and operationally complex parts of the lending lifecycle. It involves continuous borrower interaction, access to personal and financial data, and often multiple third-party agencies.

With the introduction of the DPDP Act, this stage will undergo a significant transformation, right from shifting from data-heavy, unstructured practices to a consent-driven, controlled, and auditable model.

Key Changes

1. Consent-driven borrower communication: All borrower interactions, including calls, SMS, WhatsApp messages, and emails, must now be backed by explicit and verifiable consent, and the borrowers must be informed about how and when they will be contacted.

2. Restricted use of borrower data: Collection teams will no longer be able to access or use unrelated personal data, secondary contact lists (friends/family), device-level or behavioral data without consent.

3. Tighter control over third-party collection agencies: Lenders working with external collection partners must ensure data-sharing agreements are compliant, only necessary borrower data is shared, and all actions are auditable and traceable.

4. Data minimisation and retention limits: Borrower data used during collections must be limited to what is necessary for recovery, not be retained indefinitely, and most importantly, be deleted once the recovery purpose is completed (unless required by law).

5. Increased transparency and borrower rights: Borrowers now have the right to know how their data is being used in collections, request correction or deletion, and raise grievances against misuse. This introduces direct accountability in collection practices.

With those being the key changes, let’s take a look at how the collections industry will be affected.

How DPDP Act affects Collections Industry

As we discussed previously, collections is one of the most data-sensitive sectors as it’s all about trying to make a successful reach to the borrower. But with the personal data being regulated now, let’s try to understand some areas that will need involvement of technology-driven solutions as we restrict the use of personal data:

1. Ethical and transparent recovery

The future of collections will be defined by ethical, transparent, and regulation-first recovery practices. Lenders and their partners will need to strictly abide by regulatory frameworks across every touchpoint, including telecalling, field visits, or digital outreach.

This means:

- Telecalling teams must be DRA-certified, ensuring trained and compliant borrower interactions.

- Field operations must follow strict verification, conduct, and visit protocols.

- Digital communication must be strictly consent-based, with borrowers having explicitly opted in via the lender.

- Elimination of aggressive or fragmented outreach.

2. Technology-driven collections

Collections will rapidly transition from manual, channel-specific efforts to fully integrated, AI-powered communication ecosystems.

Modern platforms will rely on:

- AI-driven communication layers (voice and conversational AI) to handle high-volume borrower engagement.

- Digital-first channels such as WhatsApp, SMS, IVR, and RCS, enabling scalable and instant outreach.

- Consent-based engagement systems, where communication is initiated only through borrower-approved channels.

Voice AI, in particular, represents a shift in how lenders interact with borrowers:

- It enables real-time, human-like conversations at scale.

- Captures borrower intent, commitments, and behavior dynamically.

- Acts as a bridge between digital nudges and human intervention.

At the same time, digital systems ensure that borrowers are contacted on channels they have already consented to, outreach is both compliant and cost-efficient, and communication is timely, contextual, and personalised.

The results in a collections engine that is not just automated, learns to become intelligent, adaptive, and borrower-aware with each engagement.

3. Higher compliance costs

As regulations tighten, lenders will inevitably face higher compliance and operational costs in maintaining audit trails to ensure agent training, consent management, and data security. However, the real shift lies in how these costs are managed.

At DPDzero, we recognise that efficient collections and compliance must go hand in hand. Our AI-powered risk engine continuously performs background analysis on borrower portfolios, profiling them into dynamic risk categories. This enables:

- Precise borrower targeting, reducing unnecessary outreach.

- Optimised channel allocation: Digital → AI → Human → Field.

- Minimisation of wasted effort and cost per account.

By ensuring that the right borrower is contacted through the right channel at the right time, we ensure every borrower interaction is fully compliant.

4. Reduced access to borrower data

Collection teams will have limited ability to access unnecessary borrower data, use secondary contact lists, and also share borrower information across multiple vendors. This will restrict traditional aggressive recovery tactics.

Inside DPDzero’s Compliance Infrastructure

For debt collection platforms, the DPDP Act is not merely a compliance requirement; it fundamentally changes how borrower data can be accessed, processed, shared, and acted upon.

Traditional collection workflows often relied on unrestricted access to borrower information across telecalling teams, field agents, and external agencies. In a DPDP-driven ecosystem, that model becomes increasingly unsustainable.

Platforms like DPDzero are built differently.

At DPDzero, compliance is embedded directly into the collections workflow through a privacy-by-design architecture, ensuring borrower data remains protected at every stage while enabling lenders to maintain recovery efficiency.

Instead of exposing sensitive borrower data across multiple operational layers, DPDzero ensures data access is governed by strict controls, auditability, and purpose-bound usage.

Here’s what that looks like in practice:

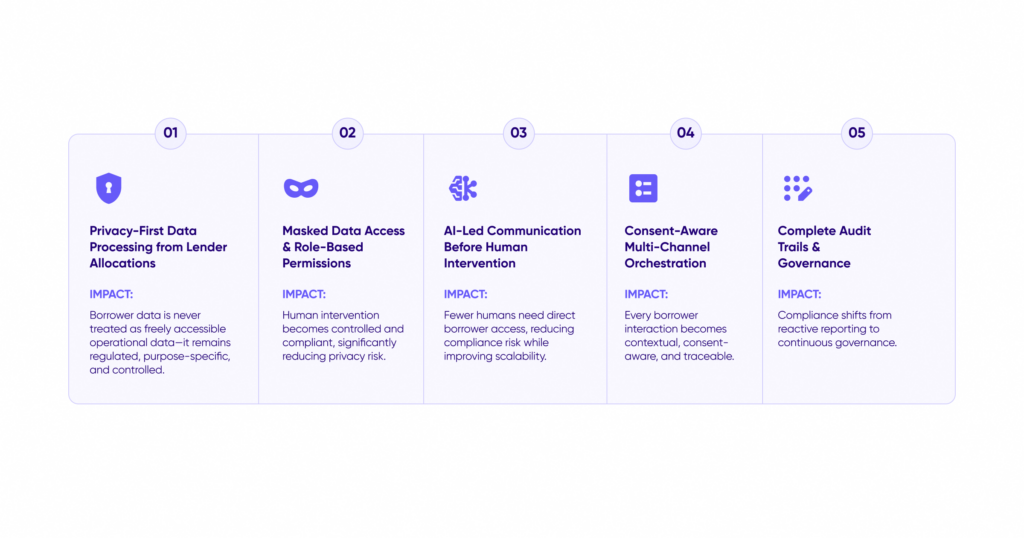

1. Privacy-First Data Processing from Lender Allocations

The compliance journey begins the moment a lender allocation enters the DPDzero platform.

Borrower data shared by lenders is processed only for the explicit recovery purpose defined in the allocation. Data ingestion pipelines are designed to ensure only the minimum necessary borrower information is made available for collections workflows.

This enables:

- Purpose-bound borrower data processing

- Data minimisation aligned with DPDP guidelines

- Controlled access across internal systems

Impact:

Borrower data is never treated as freely accessible operational data, it remains regulated, purpose-specific, and controlled.

2. Masked Data Access & Role-Based Permissions

One of the biggest compliance risks in collections is unrestricted human access to borrower PII.

At DPDzero, sensitive borrower information such as phone numbers is masked by default.

Telecallers, agents, and operational teams do not get direct visibility into borrower phone numbers or sensitive identifiers unless explicitly required and permissioned under workflow controls. Access to borrower data is governed using role-based permissions, ensuring each stakeholder only sees the data necessary for their function.

This ensures:

- No unrestricted exposure of borrower PII

- Reduced risk of data leakage or misuse

- Stronger internal access governance

Impact:

Human intervention becomes controlled and compliant, significantly reducing privacy risk.

3. AI-Led Communication Before Human Intervention

To reduce unnecessary human exposure to borrower data, DPDzero prioritises AI-led engagement across the recovery lifecycle. Digital channels and Voice AI handle a significant portion of borrower communication before escalation to human agents.

This means:

- AI handles early-stage outreach at scale

- Borrower interactions remain consistent and compliant

- Human intervention is reserved for high-complexity cases

Impact:

Higher engagement with up to 35-50% response rates and significantly improved borrower experience that lies in line with the DPDP guidelines.

4. Consent-Aware Multi-Channel Orchestration

Borrower communication can no longer be indiscriminate.

DPDzero’s orchestration engine ensures communication happens only through approved and compliant channels such as:

- SMS

- IVR

- Voice AI

- Telecalling

Channel selection is dynamically governed by borrower consent, engagement history, and communication preferences.

This prevents excessive outreach, channel fatigue, and not importantly non-compliant borrower contact.

Impact:

Every borrower interaction becomes contextual, consent-aware, and traceable.

5. Complete Audit Trails & Governance

Under DPDP, compliance requires provability, not just intent.

Every action within DPDzero is logged and auditable:

- Who accessed borrower data

- Which channel was used

- When communication occurred

- What borrower response was captured

- Which workflow triggered escalation

With real-time dashboards and governance controls, lenders gain full visibility into collection operations.

Impact:

Compliance shifts from reactive reporting to continuous governance.

Penalties for Non-Compliance with DPDP Act

The DPDP Act isn’t just another rule that companies operating in India can bypass. It’s the brick-and-mortar of what’s assumed to be the next wave of user data protection, and not just the lending industry, but every single entity in India, irrespective of the sector they operate in, has to abide by it.

And if you fail to build on top of a compliant system, the penalty for data breach in India can be extreme. Let’s see what possibly can happen:

1. Strong financial penalties for non-compliance: The Act introduces strict penalties of up to ₹250 crore, signalling a clear shift toward serious enforcement of data protection obligations.

2. Centralised enforcement mechanism: The Data Protection Board of India acts as the primary authority, responsible for investigating breaches and imposing penalties.

3. Penalties extend beyond major breaches: Even routine lapses such as lack of valid consent, unclear notices, or excessive data retention can lead to enforcement action.

4. Context-based penalty framework: Penalties are determined based on factors like severity, duration, impact, and mitigation efforts, ensuring proportional enforcement.

5. Need for strong governance and consent systems: Organisations must adopt robust data governance, consent management, and grievance handling processes to minimise regulatory risk.

What’s next for Lenders?

The shift driven by the Digital Personal Data Protection Act 2023, is clear: the future of lending will be privacy-first, transparent, and borrower-centric. For lenders and collection partners, this is not just about adapting to regulation, but about rethinking how data is used across the lifecycle.

DPDzero is built for exactly this shift, right from offering a privacy-by-design, fully compliant collections infrastructure that enables lenders to scale without compromising on data protection. If you’re preparing your systems for a DPDP-driven future, DPDzero’s Full Stack Collections Platform (Digital, Voice AI, TeleCalling, and Field operations) can help ensure:

- Every borrower interaction is data-driven and personalised

- Every channel operates within a compliant, consent-based framework

- Every decision is optimised for cost, efficiency, and recovery outcomes

In a world where collections are becoming more regulated, more digital, and more borrower-centric, DPDzero isn’t just enabling lenders to keep up; they are helping them lead the transformation.

Drop us a mail at business@dpdzero.com or sign up via the link, and we will reach out to you.

FAQs

Can I request data deletion under the DPDP Act with an online service?

Yes. Under the Digital Personal Data Protection Act 2023, individuals can request the deletion of their personal data. If consent is withdrawn or the data is no longer needed for its original purpose, the service provider must delete it unless retention is required by law.

Software solutions for managing data privacy under Indian law.

Organisations often use consent management and privacy compliance platforms to collect user consent, manage data requests, maintain audit logs, and implement data retention policies required under the Digital Personal Data Protection Act 2023.

What are the core principles of the DPDP Act?

The key principles include consent-based processing, purpose limitation, data minimisation, accountability, and protection of user rights such as access, correction, and deletion of personal data.

What is the DPDP Act and how does it impact data privacy in India?

The Digital Personal Data Protection Act 2023 regulates how organisations collect, process, and protect personal data in India, while granting individuals stronger rights over their information and introducing penalties for non-compliance.

How to check if a service provider follows DPDP Act guidelines?

Look for a clear privacy policy, consent notices, options to access or delete data, and a grievance contact. Complaints can ultimately be addressed by the Data Protection Board of India.